FTX, the bankrupt cryptocurrency exchange, is slated to appear in Delaware Bankruptcy Court on Wednesday, September 13, to seek approval for the liquidation of $3.4 billion in Bitcoin and crypto assets. The event has raised concerns among market analysts and participants, who fear that the sale could put significant selling pressure on an already struggling market.

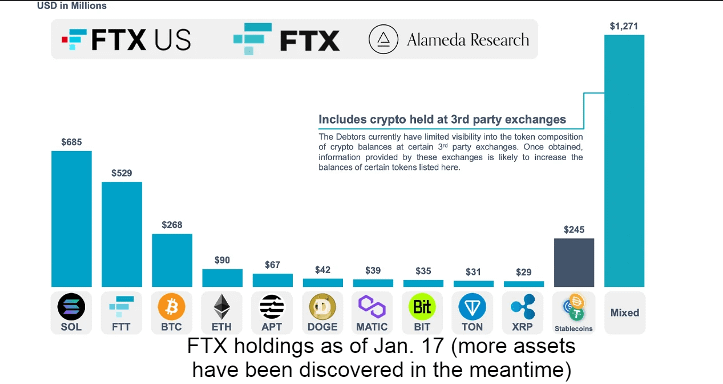

As of January 17, FTX’s crypto holdings were estimated to include $685 million in locked Solana (SOL) tokens, $529 million in FTT tokens, $268 million in Bitcoin (BTC), $90 million in Ethereum (ETH), and various other assets including Aptos ($67 million), Dogecoin ($42 million), Polygon ($39 million), XRP ($29 million), and stablecoins. An additional $1.2 billion is held in crypto on third-party exchanges.

Is A Selloff Looming For Bitcoin And Crypto?

On August 24, FTX proposed a plan to appoint Mike Novogratz’s Galaxy Digital as the investment manager responsible for overseeing the sale and management of these recovered assets. According to the plan, FTX would be allowed to sell up to $100 million worth of tokens per week, a limit that could be increased to $200 million on an individual token basis. While these propositions are not yet legally binding, they are expected to be reviewed and possibly approved by the Delaware Bankruptcy Court on September 13.

The market’s primary concern is the potential impact of these sales. Billions of coins could hit the market in the creditor sale, and there is widespread fear that the market may only recover once this overhang has been gradually eliminated. However, it’s crucial to separate fact from fiction in this scenario.

First, it’s highly unlikely that these coins will be sold en masse on the open market. Second, there is the proposed limit per week. Third, it is highly likely that most coins will be sold Over-The-Counter (OTC), and those that aren’t will be sold gradually via market makers.

Looking at the holdings, it becomes clear that a huge chunk of tokens is in FTT and Solana. Remarkably, FTX’s SOL holdings are locked and will only be fully vested in 2025 or later (until 2028). Any sale would involve a buyer taking over FTX’s vesting contract.

While FTX’s FTT tokens are marked at $529 million, their current market cap is only $350 million, raising questions about who would buy this significantly devalued asset. As for Bitcoin and Ethereum, the amounts held by FTX are substantial but not large enough to cause market-wide disruptions. Aptos, with a market cap of $1.17 billion and $67 million worth of APT to be sold, is the only asset that could potentially cause concern, but only if it is sold all at once, which is unlikely given the intent to maximize value.

Moreover, even if the court grants approval for the asset sale on September 13, the actual sale won’t commence immediately. Regulatory bodies like the SEC and CFTC are expected to oversee the sales, ensuring they are conducted in a manner that doesn’t harm investors. An underwriter will likely manage the liquidation process, ensuring compliance with all laws and regulations. This process, which involves risk assessment and finding suitable buyers, is expected to span several months.

In summary, while there will be some sell pressure, a sudden and massive sell-off is both illegal and improbable. The fear and uncertainty (FUD) surrounding the event seem to be more damaging than the event itself. Bitcoin and crypto market participants are urged to stay informed and avoid succumbing to panic and misinformation.

As a result of the rumors, the SOL price plummeted by more than 7% yesterday. The Bitcoin price saw a slight downward movement and was trading at $25,859 at press time.

Source: https://bitcoinist.com/will-ftx-liquidate-3-4-billion-in-bitcoin-crypto/